http://www.marketwatch.com/story/alibaba-will-bounce-back-just-as-google-and-facebook-did-2015-03-17?page=

If you missed out on the huge jump in the shares of Chinese online retailer Alibaba shortly after its initial public offering last year, now you have a second chance to buy.

Alibaba BABA, +0.48% has been hit by bad news, falling 30% from its post-IPO highs, to trade recently at around $84.

But here’s the key: The “bad” news really isn’t all that bad. (MarketWatch’s Jeff Reeves has a differing opinion on this.) However, it has Wall Street analysts lowering ratings, and trimming earnings and price targets. That shakes out the “momentum” crowd, which cares more about short-term noise than long-term fundamentals.

But focusing on the favorable long-term trends during pullbacks is how you make money at founder-run companies that dominate their sectors and benefit from several macro trends. Sooner or later, those kinds of companies stumble. But the favorable long-term trends ultimately win out.

That was the case several times along the way with Google GOOG, -0.09% Amazon AMZN, -0.22% and Facebook FB, -0.09% as the shares of those founder-run giants got hammered because of hiccups in the business. Applying the “long-term” mantra during their pullbacks, I suggested Google at about half its current value in late 2012, Amazon at less than half its current value in late 2011, and Facebook at a third of its value in the spring of 2013 — in my stock newsletter “Brush Up on Stocks” and in investing columns.

They did fine. And now, with Alibaba, we get to do that all over again.

Here are the three Alibaba “problems” bugging investors, and why they really aren’t that bad. Then we’ll take a look at five factors favoring this dominant Chinese online retailer.

“Problem” No. 1: There’s a big lockup release coming.

Lockup releases are the first time after IPOs that big shareholders, typically early investors and top managers, get a chance to dump stock. This one’s a biggie. On March 18, insiders will get the green light to dump 429 million shares, calculates Goldman Sachs GS, +1.35% analyst Piyush Mubayi.

That sounds frightening, since it’s almost 27 times average daily trading volume of 16 million.

But lockups often create buying opportunities. Stocks tend to be weakest around the 10 days before and after a lockup release. Often the low point happens before the lockup release, as nervous investors sell ahead of it. But there’s no guarantee, since we don’t know how much stock will hit the market. Big picture, this is a temporary negative, though. (The really big lockup release comes on Sept. 20, when 1.58 billion shares can be sold.)

“Problem” No. 2: Alibaba missed earnings estimates.

To understand this company, you need know about two key metrics. First: gross merchandise value (GMV). That is the value of all the stuff sold on its platforms and, importantly, not out of inventory. Alibaba’s two main platforms, Taobao Marketplace and Tmall.com, are like eBay EBAY, -0.35% and Amazon’s third-party vendor business, respectively, in that they carry no inventory.

Instead, Alibaba makes money on sales commissions and by auctioning key search words and banner advertising. The next metric is the “take rate,” or all of that income divided by GMV.

Alibaba’s stock is now weak, in part, because its take rate just took a hit. But it’s declining for a good reason: Alibaba is selling more stuff than expected on mobile phones. The take rate on phone-based sales is lower than that on PC-based sales — for now, at least. So the bigger-than-expected shift to mobile weighed on the take rate.

Two things to keep in mind here. First, the faster-than-expected transition to mobile is a good thing. Chinese consumers are flocking to mobile, and you wouldn’t want to see Alibaba left behind. Second, Alibaba’s mobile take rate has been expanding rapidly, and that trend is going to continue, so it will catch up to the PC take rate. The take rate in mobile has grown to about 2% from 0.44% in June 2013, and the PC take rate is 3.2%.

“We think Alibaba will monetize the mobile take rate efficiently and close the gap,” says Di Zhou, associate portfolio manager at Thornburg International Value Fund TGVAX, +0.92% which has outperformed competitors by 1 percentage point a year, annualized over the past decade.

Interestingly, Facebook had a similar negative during its early transition to mobile. Its profitability metrics lagged behind for similar reasons. That’s partly why its stock drifted down toward $20 in its early days. But Facebook managed the transition to mobile well, as Alibaba will.

Alibaba’s take rate on PC-related sales dipped in the most recent quarter to 3.2% from 3.5%, another reason for the negativity on the stock. But it has been growing rapidly and the recent decline is partly because Alibaba is changing how it prices key search words purchased by advertisers. The changes should benefit the company in the long term, says Credit Suisse analyst Dick Wei.

Problem No. 3: It looks like the government is trying to crack down on fake products

Alibaba shares took a hit recently when a government agency singled out the company for having counterfeit goods on its websites. Alibaba challenged the study, and the government took it down. But since counterfeit goods are a significant part of the retail market in China, the skirmish has investors worried.

This may not wind up being a big problem. There’s some logic to Alibaba’s defense that it is just a platform for other sellers, and that it’s up to the government to police those sellers, not Alibaba. It’s a task that would be pretty tough for the company anyway, since well over $100 billion worth of stuff was sold on its platforms last quarter. It’s also a job that’s going to be hard for the government, given the prevalence of counterfeit goods in China’s consumer culture.

On the following page are five factors that should help push Alibaba’s shares much higher over the next few years.

Reason No. 1: Consumer-spending growth in China is phenomenal.

A lot of people are joining the middle class in China. So retail spending is growing at a robust 10% to 12% a year, Thornburg’s Zhou points out.

Reason No. 2: E-commerce in China is still in the early stages.

China doesn’t have a lot of stores, compared with more developed areas of the world. That’s a plus for e-commerce, which is growing much faster than overall retail sales. “There are billions of people who are becoming consumers and they don’t have a Walmart WMT, +1.70% but they have a cell phone,” says Kevin Carter of Big Tree Capital, which invests in emerging and frontier markets.

Reason No. 3: Alibaba is the big dog in the industry.

Alibaba’s Taobao Marketplace and Tmall.com dominate their respective areas of retail. Both eBay and Amazon have tried to enter China, and it did not go well. Tellingly, instead of operating independently, Amazon just set up a store on Tmall.com. About 86% of the stuff bought on mobile phones is purchased on Alibaba platforms, the company says in filings.

Reason No. 4: Alibaba’s growth is phenomenal.

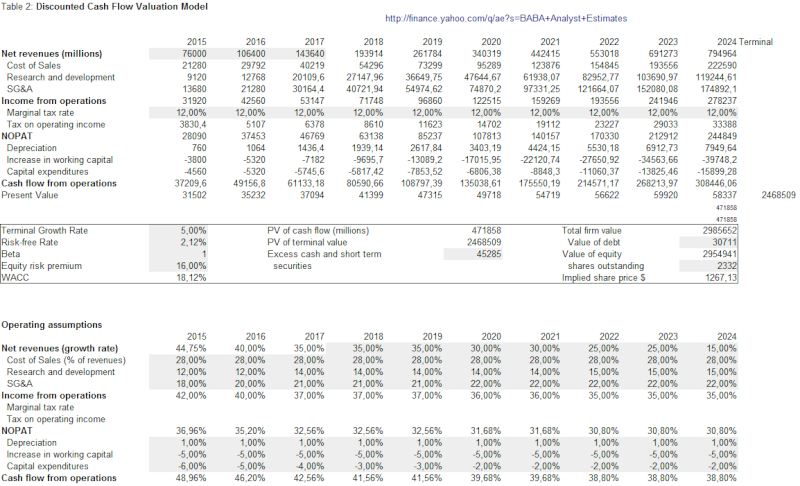

The value of stuff sold on Alibaba platforms, that GMV, grew by 49% last quarter, compared with the year before. Sequential growth was 42%. Revenue grew 40% over the prior year and 56% sequentially. “There are very few companies that have existed that are this size and growing this fast,” Carter says.

The number of shoppers on Alibaba platforms rose 45% from a year earlier to 334 million. That’s still only half the number of people who are online in China, and a quarter of the overall population, according to Jason Moser at Motley Fool. “There is such a tremendous market opportunity there,” he says.

Reason No. 5: Alibaba is founder-managed.

I always like companies managed by their founders because studies show they outperform — probably because that entrepreneurial drive never really wears off in people even as they become wildly successful. That continues to help those companies thrive more than companies run by professional managers. That’s certainly been the case with the biggest founder-run Internet success stories like Google, Facebook and Amazon. Alibaba co-founders Jack Ma and Joseph Tsai still help run the company via leadership positions on its board.

I’d buy Alibaba as a multiyear holding, but given the recent sell-off, you could do well even if you have a shorter time horizon. Wei, at Credit Suisse, thinks the stock will rise to $114 in a year — for a potential 40% gain.

At the time of publication, Michael Brush had no positions in any stocks mentioned in this column. Brush is a Manhattan-based financial writer who publishes the stock newsletter “Brush Up on Stocks.” Brush has covered business for the New York Times and The Economist group, and he attended Columbia Business School in the Knight-Bagehot program.

Início

Início